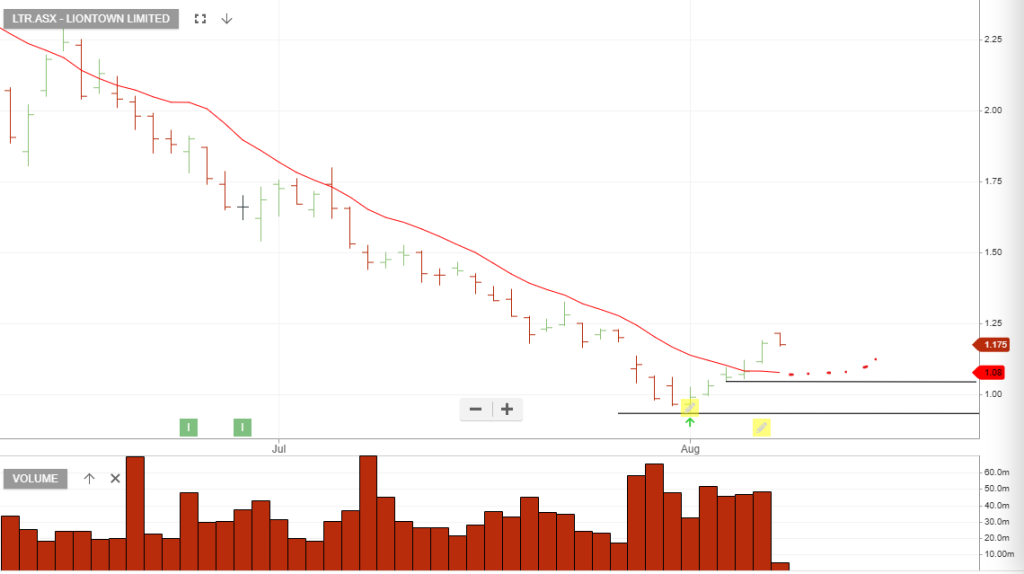

Liontown

Pexa

Nasdaq Top 30

Lynas Rare Earths

Iluka

Fortescue

ASX:FMG should be on your watchlist. We’re waiting for further buying confirmation.

Lynas Rare Earths

Liontown

Pexa

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453