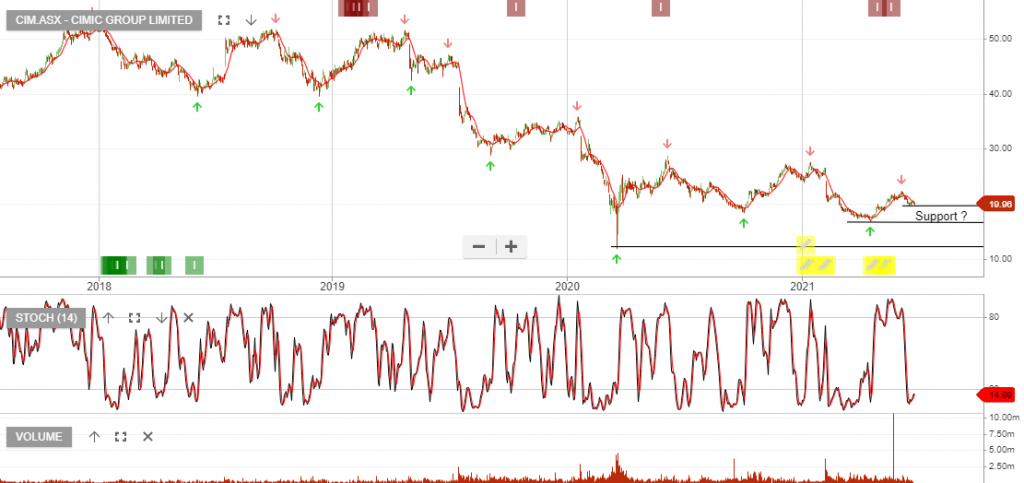

Cimic Group is under Algo Engine sell conditions. Despite this, we’ve held a view that the company has cleaned up the balance sheet and offers exposure to an increasing infrastructure build thematic.

The FY20 earnings result and FY21 guidance was below market consensus and we’ve seen the stock sell off as a consequence.

FY21 NPAT guidance of $400-430m down from FY20 NPAT of $600m.

The silver lining is the business does appear to be de-risking and likely to manage its way through the transition to new, lower risk contract wins.

The forward yield is now 4%, but the free cash flow generation will need to be watched closely.

Cimic Group has been one of our high conviction ideas expressed to members during our regular Monday night webinars.

CIM offers exposure to above-average EPS growth supported by increased government and private spending on infrastructure in Australia, New Zealand and Asia.

CIMIC is scheduled to report full year earnings on 10 Feb with NPAT estimated to be around $650mil.

Cimic Group has been one of our high conviction ideas expressed to members during our regular Monday night webinars.

CIM offers exposure to above-average EPS growth supported by increased government and private spending on infrastructure in Australia, New Zealand and Asia.