A number of stocks within the ASX top 50 appear to be setting up medium term short signals.

We’re mindful of the upward bias in equity indexes, however, much of this is driven by broad inflows into index funds and valuations are becoming stretched, even if Q1 earnings in the US hit their target.

Here is a list of the names that are worth taking a closer look at….

We generally don’t participate on the buy-side when it comes to options on individual stocks. However, we do buy index options to hedge portfolios or to make profits on short-term corrections.

In the current environment, when some stocks look overvalued, it makes sense to buy put options on a stock specific basis.

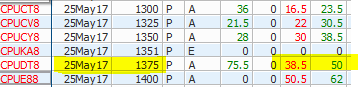

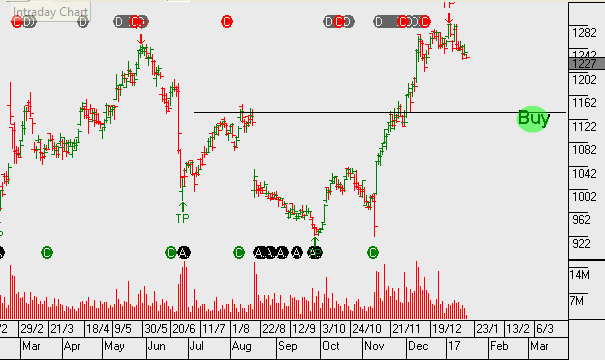

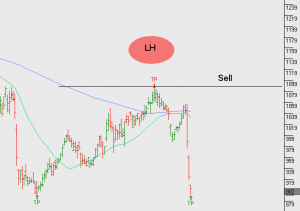

Let’s track these over the weeks ahead as a strategy to profit from a pull-back in the share price of CPU.

Over recent weeks, we’ve highlighted a number of stocks that are overvalued and susceptible to any increase in market volatility or risk-off period.

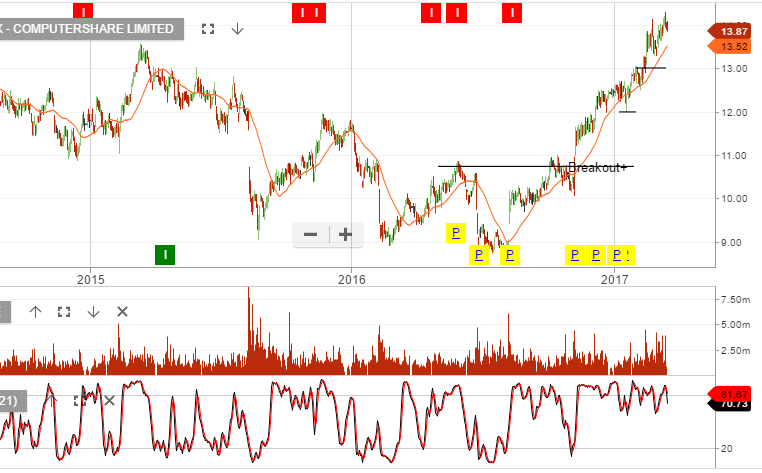

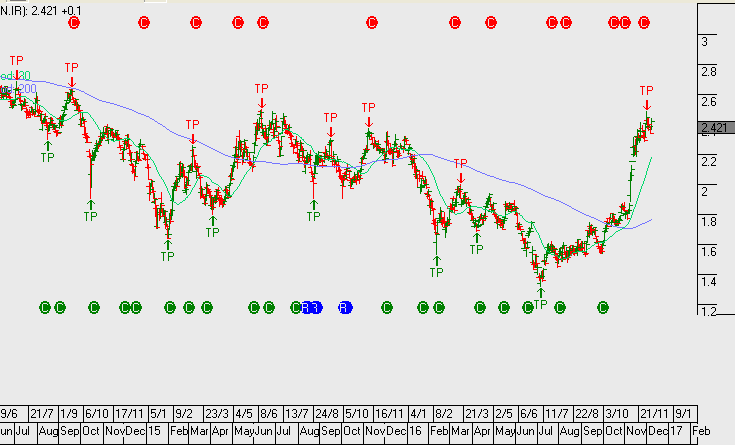

Stocks that have rallied due to higher US interest rates are starting to retreat as the yield on the US10-YR starts to slip lower from the recent 2.64% high. Companies affected in this group include Computershare and QBE.

Australian Banks are beginning their sell-off and our bank hedge is starting to pay-off.

Exiting property plays, especially where there’s development risk will likely prove worthwhile in the coming months. We’re happy to stay exposed to the best-of-the-best only in this space and sell tight covered calls.

The issue we see is that the US bank results out so far, is probably as good as it gets for US 4Q earnings. Over the next two weeks, multinationals, industrial names and then big technology will announcement their results.

If we see an average EPS run rate for the S&P500 that fails to meet the $132 per share expectations, and in fact averages somewhere in the range of $120 – $125, then the Dow Jones will struggle to move higher.

With the above in mind, we’ve been making adjustments to portfolios to hedge an uptick in volatility and deliver returns through an aggressive derivative overlay.

Currently, ASX leading Financials are being dragged higher as the US equity rally continues into the lead up to their fourth quarter earnings results. We’re somewhat sceptical of the valuation support and yesterday started hedging our banking exposure in client portfolios. This was done through using in-the-money European-style calls over CBA and slightly in the money February calls over NAB, as two examples.

In the case of CBA, we stay exposed to the February dividend and franking credit but have hedged a price pullback of up to 5% between now and March.

In NAB, we’ve hedged to a similar extend but without the need to protect the dividend. NAB’s next payment period is not until May

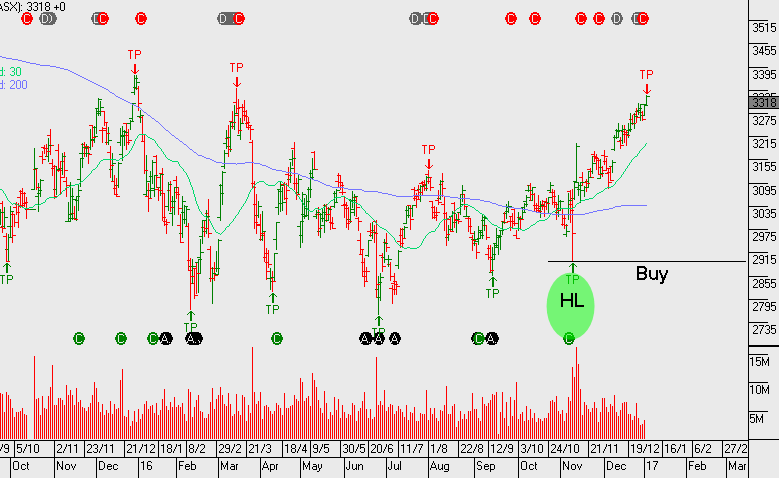

Computershare and QBE Insurance are experiencing strong rallies at present, the catalyst being higher interest rates in the US. The FOMC meeting on the 14th of December may provide a short term cap in the bond yield rally, if this occurs QBE and CPU will likely run into resistance.

At yesterday’s AGM, Computershare gave guidance for FY17 which suggests the group has found an inflection point in their earnings. After almost 2 years of earnings downgrades and underperformance, management is increasingly looking towards mortgage servicing for growth, as the mature share registry business faces structural pressure.

CPU guided towards FY17 EPS to be marginally up on FY16. Contribution from Mortgage Servicing is required to deliver the growth.

Forecast FY17 revenue $2b on EBIT of $500m, EPS of $0.57 and DPS of $0.27 placing the stock on a forward yield of 3.3%.

We continue to remain cautious and question the certainty of a sustained turnaround in earnings. We continue to watch this name from the short side. The algorithm engine will be tracking CPU for a short signal as the market bounces back after the post Trump victory rally.

CPU.ASX reported FY16 earnings of US$0.55 per share in line with guidance and down almost 8% on the same time last year. The result was impacted by a higher tax rate which masked what looks to be a moderate improvement in the underlying business and this is reflected in managements FY17 guidance of a return to 1 – 3% EPS growth.

Based FY17 expected earnings it places CPU.ASX on a 3.6% dividend yield and we still have questions around certainty of earnings growth out into FY18 and FY19.