Downer EDI

Downer EDI continues to trade higher and the stop loss can be lifted to $4.11

Downer EDI continues to trade higher and the stop loss can be lifted to $4.11

Downer EDI is now an open trade with a stop loss below the pivot low.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

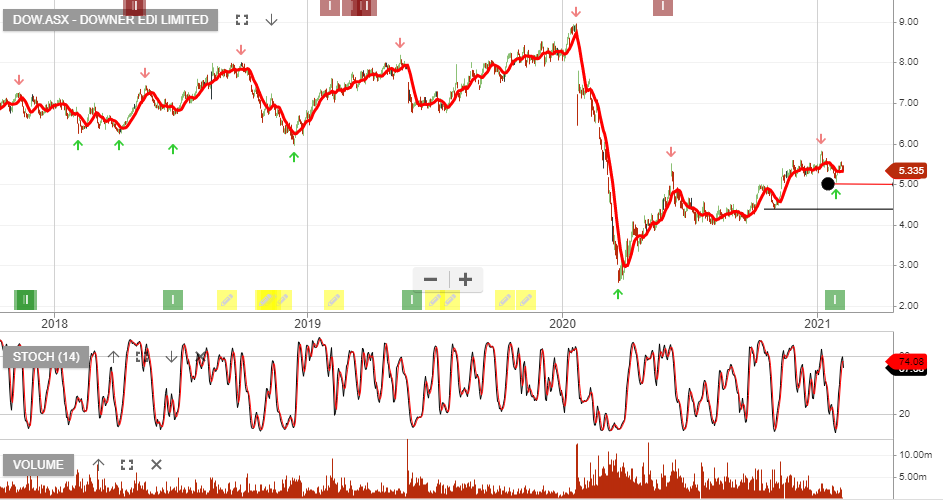

Downer EDI is now under Algo Engine buy conditions, following the entry signal at $5.15. The stock is now included in our ASX 100 model portfolio.

The company is making progress on its urban growth strategy and the divestments within the mining services sector are helping to sure up the balance sheet and de-risk the business outlook.

We see scope for double digit EPS growth into FY22 & FY23.

,

Downer EDI is now under Algo Engine buy conditions, following the entry signal at $5.15. The stock is now included in our ASX 100 model portfolio.

The company is making progress on its urban growth strategy and the divestments within the mining services sector are helping to sure up the balance sheet and de-risk the business outlook.

We see scope for double digit EPS growth into FY22 & FY23.

,

Downer EDI is now under Algo Engine buy conditions, following the entry signal at $5.15. The stock is now included in our ASX 100 model portfolio.

The company is making progress on its urban growth strategy and the divestments within the mining services sector are helping to sure up the balance sheet and de-risk the business outlook.

We see scope for double digit EPS growth into FY22 & FY23.

,

Downer EDI is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

The company reaffirmed FY20 net profit after tax guidance of $365m, which represents 7% growth on the same time last year.

Dow trades on a forward yield of 3.7%.

We see value in accumulating the stock within the $7.50 – $8.00 price range.

Level 29 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453

Or start a free thirty day trial for our full service, which includes our ASX Research.