James Hardie 1Q 24 Earnings

James Hardie Industries 1QFY24 NPAT increased 14% and guidnace for the 2Q was upgraded to US$170-190m. The key positive is USA growth and margin expansion.

We’re looking to JHX on the next Algo Engine buy signal.

James Hardie Industries 1QFY24 NPAT increased 14% and guidnace for the 2Q was upgraded to US$170-190m. The key positive is USA growth and margin expansion.

We’re looking to JHX on the next Algo Engine buy signal.

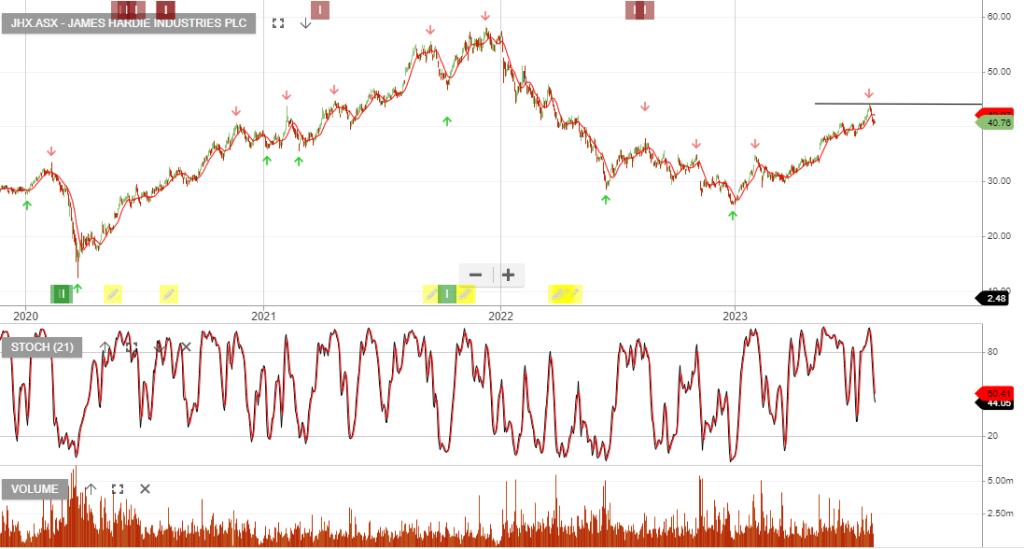

James Hardie Industries is approaching an oversold range where investors should begin monitoring the short-term momentum indicators for a pick-up in buying activity.

James Hardie Industries is approaching an oversold range where investors should begin monitoring the short-term momentum indicators for a pick-up in buying activity.

The price range for a reversal in price action remains wide at $33 to $39.

James Hardie Industries is approaching an oversold range where investors should begin monitoring the short-term momentum indicators for a pick-up in buying activity.

The price range for a reversal in price action remains wide at $33 to $39.

James Hardie Industries is approaching an oversold range where investors should begin monitoring the short-term momentum indicators for a pick-up in buying activity.

The price range for a reversal in price action remains wide at $33 to $39.

James Hardie Industries is approaching an oversold range where investors should begin monitoring the short-term momentum indicators for a pick-up in buying activity.

The price range for a reversal in price action remains wide at $33 to $39.

James Hardie Industries was added to our model portfolio last month and is now up 13.5%

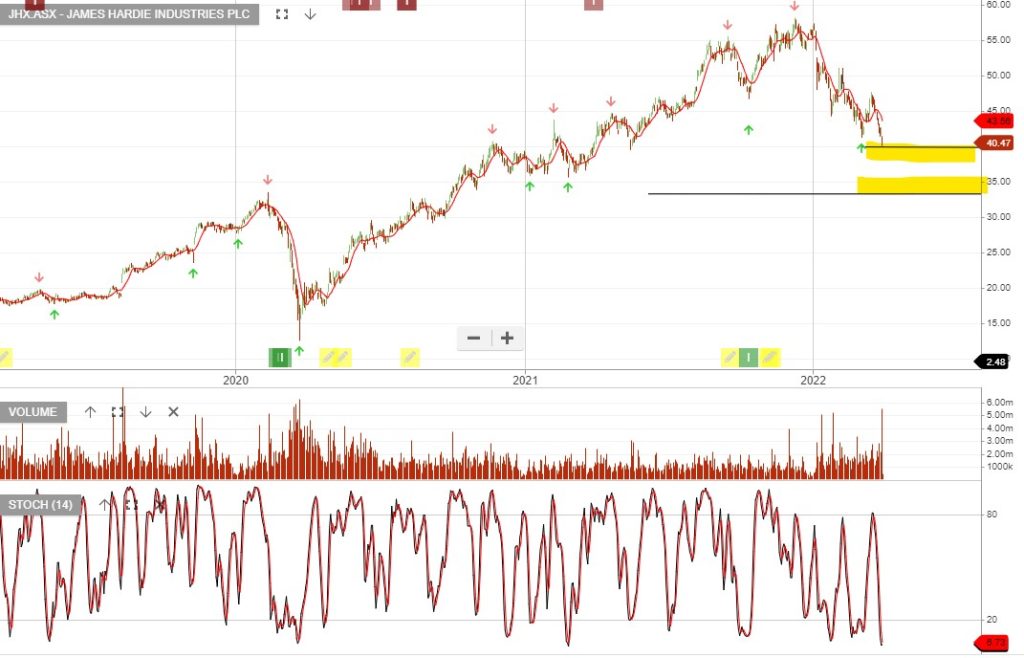

FY22 Guidance range has been upgraded from USD550-590m to USD580-600m.

After 20% growth into FY22 and FY23 analysts are forecasting slower growth of 10% in FY24. The stock trades on a forward yield into FY23 of 2.5% and a forward PE of 25x earnings

James Hardie Industries was added to our model portfolio on 12 October and is now up 14.6%.

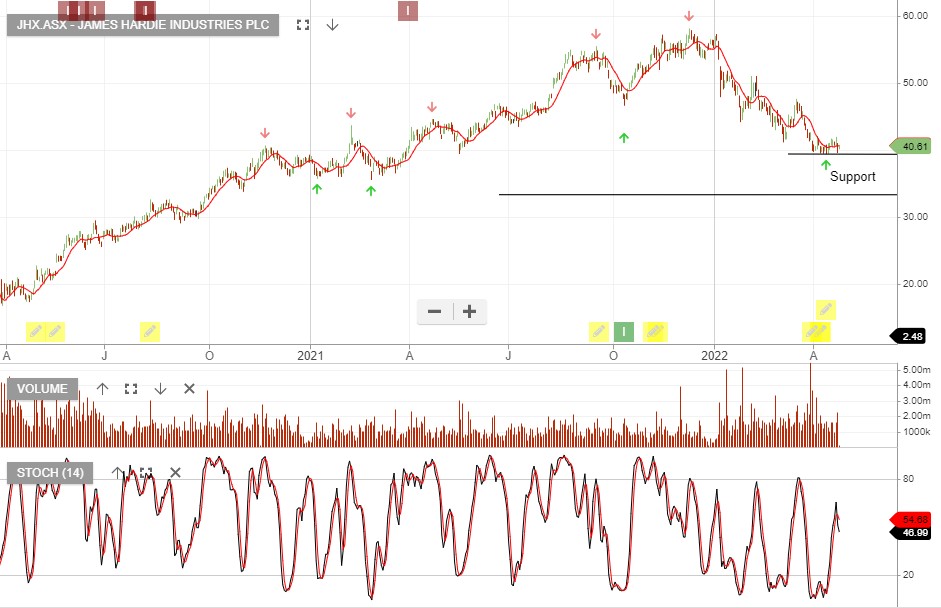

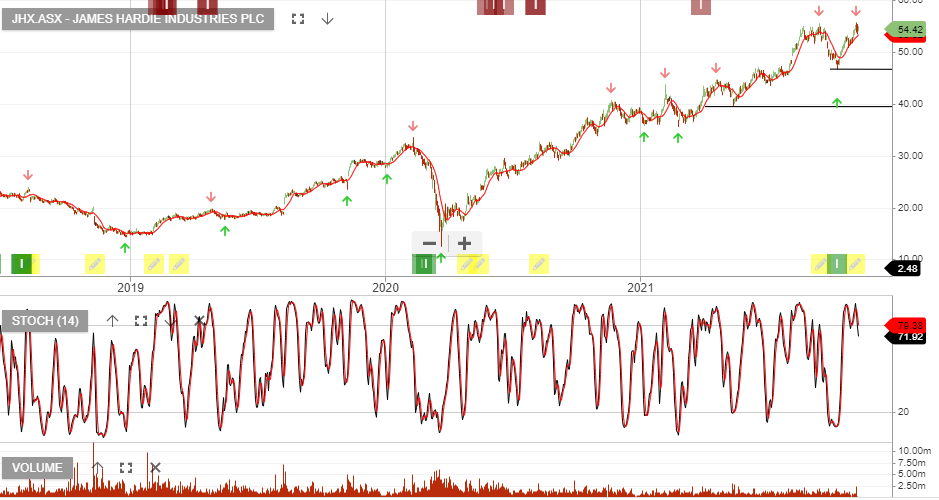

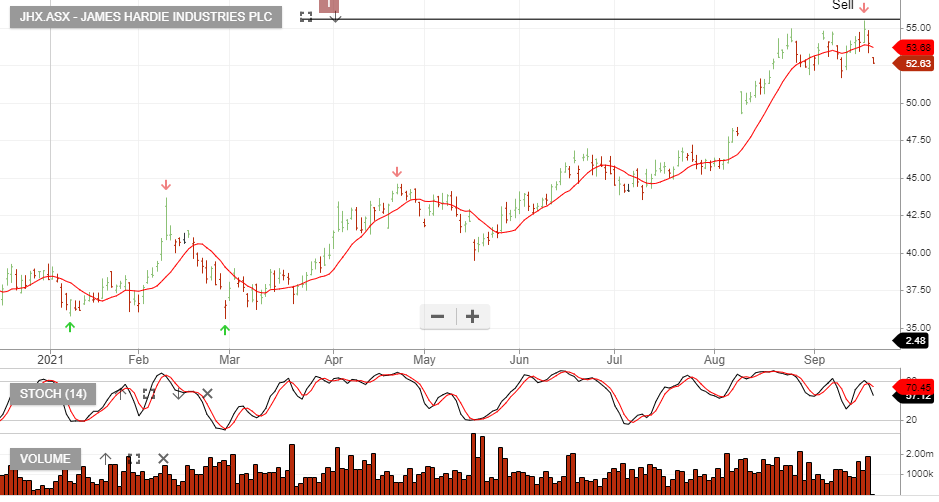

James Hardie Industries is under Algo Engine sell conditions and we expect selling pressure to build with overhead resistance at $55.00.

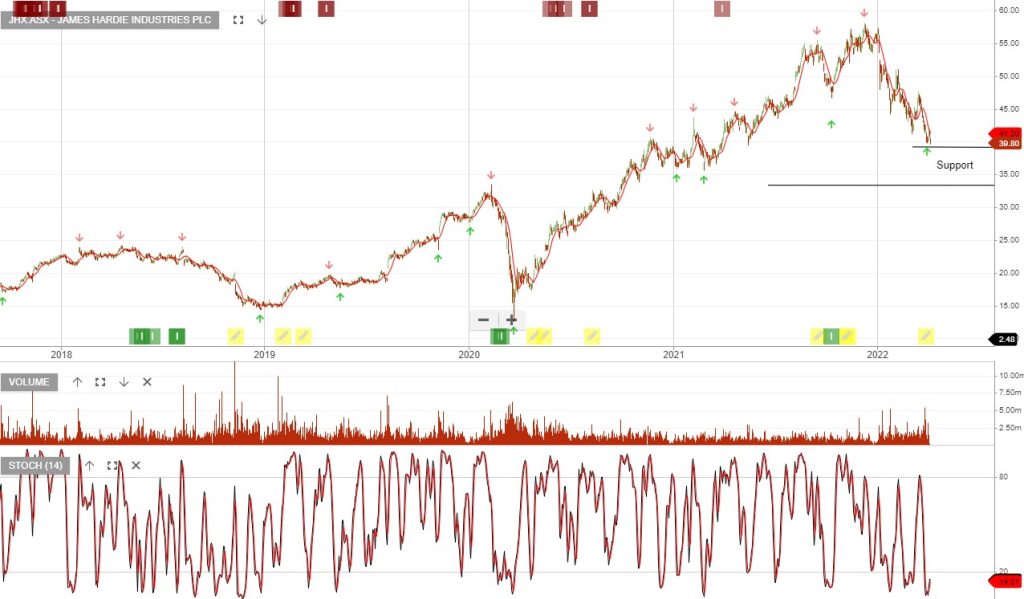

James Hardie Industries FY21 profit guidance now stands at $US330m-$US390m. June quarter earnings were flat on the same time last year.

Level 29 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453

Or start a free thirty day trial for our full service, which includes our ASX Research.