Ramsay Health Care

Ramsay Health Care Buy with a stop loss at $35.10

Ramsay Healthcare

Ramsay Health Care has formed a higher low at $35.

Ramsay Healthcare

Ramsay Healthcare

Ramsay Healthcare

Ramsay

Ramsay Healthcare

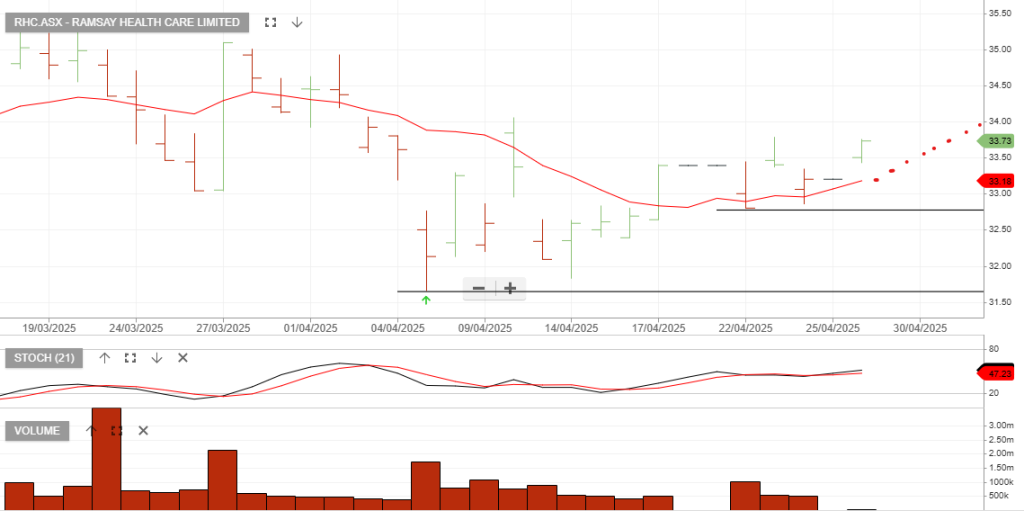

Ramsay Health Care is rated a buy with the stop loss at $32.80

Ramsay Healthcare

Ramsay Health Care has been upgraded to Outperform by Macquarie Bank.

Ramsay Healthcare

Ramsay Health Care is rated a buy.

Investors demand Ramsay to spin off or sell offshore assets and focus on Australian business operations.

Ramsay reported $16.8 billion in revenue and $270.6 million in profit after tax in the year to June 30. Profit dropped 2.7 per cent.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453

Send our ASX Research to your Inbox

Or start a free thirty day trial for our full service, which includes our ASX Research.